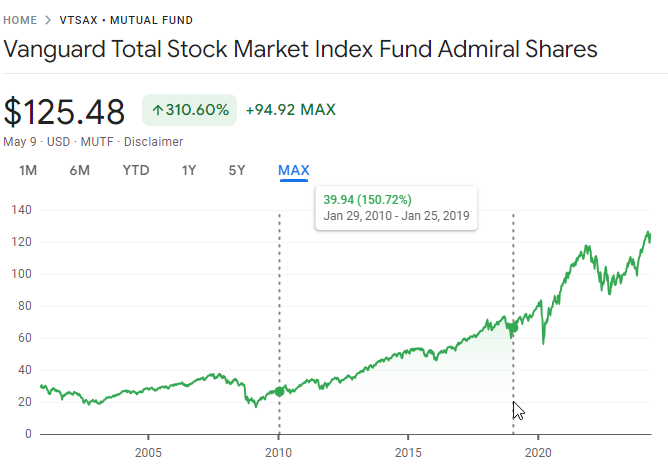

It took a long time before I have adapted to the way I invest and I believe it will keep evolving. Back in 2010, I made my first investment following the advice of a book for dummies. It was my first book that I read which got me started on a path to become more financial literate. All I did was put a good lump sum of money in the total stock index because

- VTSAX was an advice in the book for great returns, not to aim to beat the market

- Going with this fund, it was a cheap way to get good a “managed” fund since it didn’t involve any fund manager

- You can set it and forget about it.

In just about 9 years from when I put in my money, it gained a whopping 150.72% and it is still growing since I put that lump sum in a Roth IRA, where I can pull out that money in retirement tax free! How lucky was I to come across the book and follow its advice!

All though all the success was there, I believe I can do better. My progression of becoming more savvy didn’t stop with a dummies book. I explored other sources of advice. That’s where my progression took me to invest differently. Since then, I’ve tried doing the Golden Butterfly to make investment in a more autopilot mode since I also have to manage my wife’s account. So this helps me set it and forget it.

I’ve also been more hands on with our choices in our 401k. I used to opt-in for the default, which is the nice Target Fund goals, where the idea is the allocation of the portfolio adjusts to less risky assets as you reach your retirement age. All though this is a good vehicle to be on (it’s also evolving as experts discover better ways to serve the generation who have a longer life span), it still suffers slightly on the fee you have to pay. These are all good for autopilot, but experts like those in Stacking Benjamins, points to its audience that it is not that hard to manage it. They recommend to at least put an extra 10% to those small cap funds because it is underrepresented.

After crushing my investment in the early years, I discovered we can go farther than our 401k and contribute also in individual IRAs. This was great because we were getting 100% match from our employer for the first 4% of our contribution to our 401k, all though the selection was limited, anything more than the 4% went to our individual IRAs where we can have a lot more freedom to pick what we want. But at this time, I kept it simple by placing the contribution in an ETF known for holding stocks that have been diligently increasing their dividend year-over-year for the last 10 years, VIG. I’m not sure where I read it but dividends stocks was the thing to focus your investments on.

If you are the type of person who likes to set it and forget it, then you can stop early and follow great advice from Paula Pant of Afford Anything or from Joe Saul-Sehy of Stacking Benjamins, where you don’t really have to beat the market, you can just be the measuring stick or part of the benchmark. There’s nothing wrong there. If you like to control some of this, you can too to get the itch off by allocating about 10% of your capital to your experimental investment strategy. This is very different from person to person and that’s why it comes back to being personal finance. Since every situation is different.

Please make sure to read our disclaimer as I’m not a financial advisor.