Being a kid, they almost don’t have to worry about anything. If they’re lucky, almost everything will be provided to them by their loving parents. They have no clue what their parents go through to be able to provide the things they need and occasionally the things they want. There isn’t much they can do with their situation until they become more independent and responsible. But I do say that starting at this very young age, they can learn a lot especially learning from our mistakes we encountered in our own lives. Teaching them our mistakes and how to avoid them and also teaching them the ways we found to be successful. Most parents would like their kids to be successful so why not instill these success in our children while they still look up at us and absorb everything we teach them.

If you’re unsure what kind of system will be good to teach your child, you can always start with a simple strategy of putting small amounts of money in different buckets or jars. You can have a minimum of three jars and up to six depending on what you consider important. This exercise is nice because we practice a basic rule and will stay with our children until they grow up and have their own family. Laying down some basic foundation can go a long way to help them prepare for the real world.

Here are some of the important things that one might consider when trying to teach a kid

- Savings

- Spending

- Sharing

- Emergency

- Charity

- College

Savings is pretty self explanatory. To be able to have a good future, we need to learn to pay ourselves first before anything else. This will allow them to train to save for big things in life and minimize the need to borrow money. A good way to encourage your young one to save is match the savings they put into this bucket. For example, if they decide to put $10 into the savings then you can match some percentage of that savings, say 2%, so you also would put $2 along with their $10. This way it enforces their behavior to save.

Spending might not be something you’d think we should teach children, but giving them the power to handle money and use it for the things they need or want may help them in the future. I would rather have my child learn from a $10 mistake on spending than a $1000 mistake when they grow up. Allowing them to experience how to spend their money sets them up in the future. Aside from teaching them to handle money, you can also help them if the spending is too high say for a school trip or a friend’s birthday gift when these unexpected things come up. You can help them by contributing some percentage of what it costs.

Sharing is the concept of taxes that they will experience when they start working for money. It’s the concept of being a citizen of the household and thus they have to give back something to the household. This sharing is for the entire family. The amount stored in sharing can then be spent on anything that the family uses like a new frying pan or a new toaster or a trip to a theme park.

Emergency is another one of those odd items on the list. What kind of emergency would a child have? Well, this again is for training purposes. At different levels of their age, they can have an emergency fund. When they’re 5 years old, then can have $50 inside their emergency fund. When they’re 10 years old, they can have $1000 in their emergency. This should never be touched ever, unless it is really an emergency. This will prepare them when they’re on their own. The would know that emergency fund is there to help them when they have an emergency.

Charity teaches your child to be humble and appreciate what they do have. It molds them as a good person to be able to donate to a cause bigger than themselves. They might find some passion on helping a cause and understand the world better.

Finally, this is for their future. They could depend on this money when they go to college for further education. It will certainly help them avoid student loans.

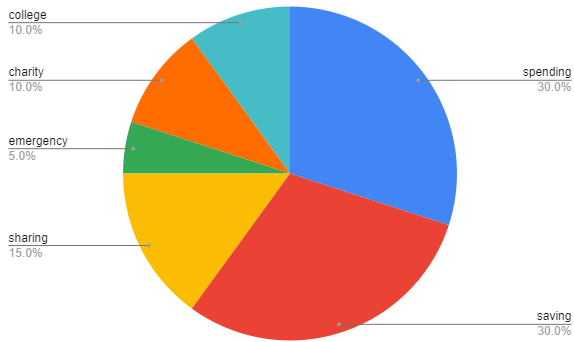

Below is a sample of how you may want to mix the 6 items

Like I said in the beginning, it’s not necessary to have all six buckets. You may have a separate way of handling college fund and emergency funds so it may not apply. But the same concept of dividing the total into small pieces of the pie. It also depends on how much you want to emphasize on item over another.

Here’s is another sample without all six buckets.

When your child is old enough, they can decide how much they want to keep for spending and put away for saving. But you must dictate how much sharing should be and as well as how much the household contribute to charity. In the end, being the parent you get the final judge to everything they do. If you think it’s not fair to assign 1% to saving, then challenge them to change it. You also have the final say on what they can blow their money on like if your household doesn’t allow for bubble gum then that has to be observed or when they want a $1000 toy, you always have the final say.

So how much money/allowance should they receive? Their age seems to be a good way to equate how much they should receive. So if your child is 5 years old, they will receive $5 weekly and if they’re 10 then $10 weekly. It’s easy to remember and would allow them sufficient money to tackle different buckets.

Final words of advice, while they are young take advantage of it. Teach them as much as you can because they will be in that age where they will listen and in the age that will help them develop to be financially responsible. The teaching goes beyond finances, so think about other things you may want your child to learn before they start making their own decisions in their teenage years.